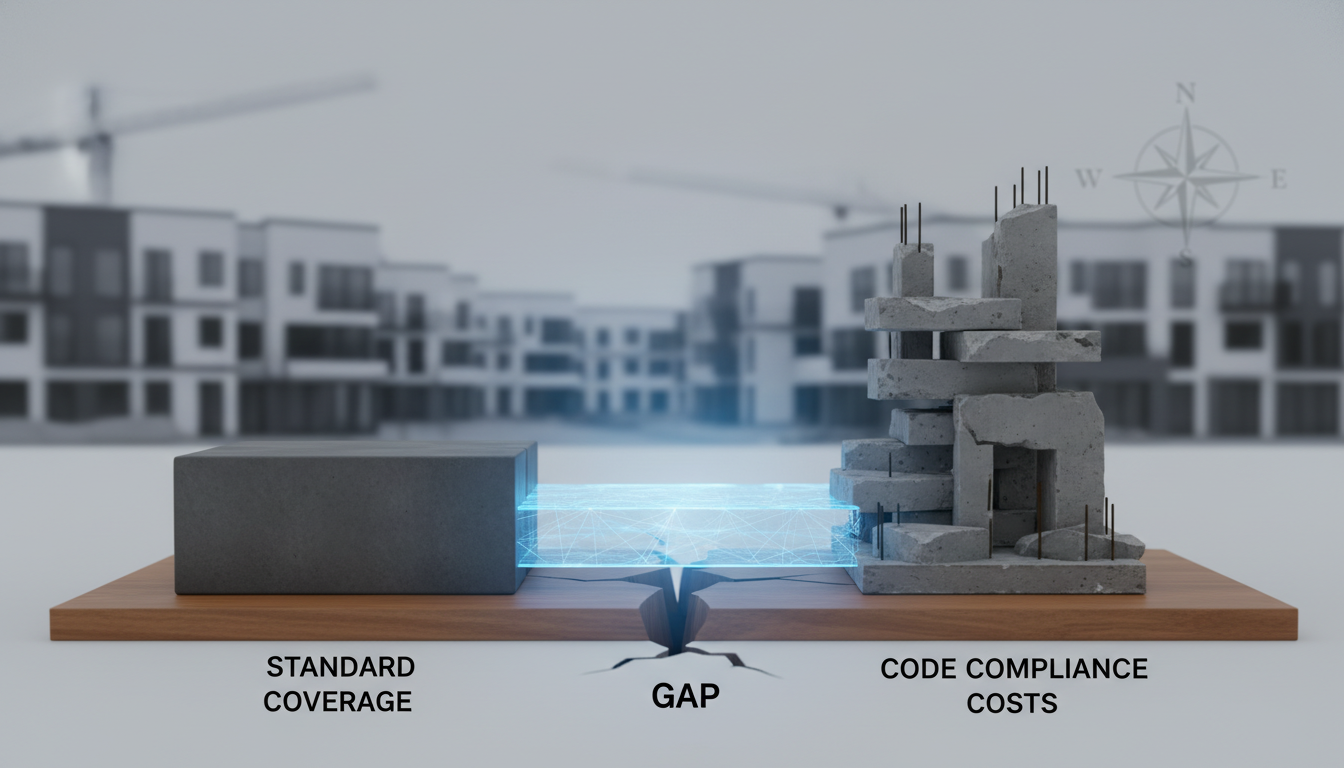

For the owners of high-value estates in the West Metro—spanning the historic corridors of Edina, the lakeside vistas of Wayzata, and the wooded retreats of Minnetonka—a property loss is more than a logistical hurdle; it is a threat to a significant capital asset. When a fire, severe windstorm, or water catastrophic event occurs, the primary objective is restoration to a pre-loss condition. However, a profound disconnect often exists between what an insurance policy promises and what local building departments require.

This gap is where “Ordinance or Law” coverage becomes the most critical component of a homeowner’s insurance portfolio. As premium insurance adjusters and high-net-worth (HNW) individuals understand, the concept of “like-kind and quality” is a double-edged sword. While it aims to return the property to its former state, it does not inherently account for the evolution of the International Residential Code (IRC) or specific municipal mandates. Without the proper endorsements, a homeowner may find themselves personally responsible for hundreds of thousands of dollars in mandatory upgrades. At Partners Restoration, we serve as both Master Builders and Certified Insurance Advocates to ensure that these “hidden” costs are fully recognized and funded by the carrier.

The Fundamental Paradox: Like-Kind Quality vs. Legal Compliance

The standard homeowners insurance policy is designed on the principle of indemnity: to make the insured whole again. In the context of a claim, this usually translates to “like-kind and quality.” If your 1950s colonial in Edina had copper plumbing and R-11 insulation, the insurer’s baseline obligation is to pay for copper plumbing and R-11 insulation.

The paradox arises when the local building inspector arrives at the site. Modern municipal codes in the West Metro have evolved significantly over the last several decades. Today’s codes may require R-49 insulation, high-efficiency HVAC venting, seismic bracing, or whole-home fire sprinkler systems. The insurer may argue that these upgrades constitute “betterment”—an improvement over the original state that they are not obligated to fund. Without Ordinance or Law insurance coverage restoration, the homeowner is caught in a financial pincer movement: the law says you must upgrade, but the policy says they won’t pay for it.

Understanding the Three Pillars of Ordinance or Law Coverage

Ordinance or Law coverage is typically broken down into three distinct parts. Understanding these nuances is essential for any adjuster or homeowner navigating a complex rebuild.

| Coverage Part | Description | Real-World Example |

|---|---|---|

| Coverage A | Loss to the Undamaged Portion of the Building | A fire destroys a significant majority of a home. Local “a substantial portion rules” require the remaining a substantial portion (undamaged) to be demolished and rebuilt to modern code. Coverage A pays for the value of that a substantial portion. |

| Coverage B | Demolition Cost | The cost to tear down and haul away the debris of the undamaged portion of the structure that must be removed to comply with local ordinances. |

| Coverage C | Increased Cost of Construction | The additional funds required to bring the rebuilt sections up to current code, such as installing required fire sprinklers or updated electrical panels. |

Geographic Risks: The “Edina a substantial portion Rule” and Beyond

In the West Metro, the risk of code-triggered cost overruns is statistically higher than in many other regions of Minnesota. This is due to a combination of aging luxury housing stock and aggressive municipal enforcement of building standards. One of the most significant hurdles we encounter is the Edina a substantial portion Rule.

Under this ordinance (and similar rules in neighboring jurisdictions), if a home sustains damage that exceeds a substantial portion of its market value, the entire structure—including the portions untouched by the initial loss—must be brought into full compliance with the most current building codes. For a sprawling estate built in the 1920s, this can be catastrophic. We have seen instances where a kitchen fire and subsequent smoke damage triggered a requirement for a full electrical overhaul of a 6,000-square-foot home. Without robust Ordinance or Law coverage, the “gap” between the fire repair and the mandatory electrical upgrade can reach six figures.

Furthermore, in areas like Minnetonka and Wayzata, environmental and shoreline regulations add another layer of complexity. Architectural Reconstruction in these zones often requires sophisticated stormwater management systems or specific setbacks that did not exist when the home was originally constructed. These are not “optional” upgrades; they are legal prerequisites for obtaining a certificate of occupancy.

The Role of Advocacy: Why Standard Adjusting Falls Short

Many independent or staff adjusters utilize automated software like Xactimate to generate repair estimates. While these tools are efficient, they are often programmed with “standard” repair templates that ignore specific local ordinances. A standard estimate might include the cost of a new water heater, but it will rarely include the cost of the expansion tank, the seismic strapping, or the specific venting required by a particular West Metro municipality.

This is where Partners Restoration provides unparalleled value. Our role is to act as a bridge between the technical requirements of the building code and the contractual obligations of the insurance policy. As Master Builders, we don’t just guess at what the code requires; we engage with local building officials early in the process to secure a written determination of what upgrades will be mandatory.

Statistical Frequency of Code-Triggered Overruns

Data from recent high-value restoration projects in the Edina and Minnetonka areas suggests that nearly a large majority of claims involving homes older than 30 years encounter at least one significant “code-trigger” that was not included in the initial insurance scope. On average, these code requirements increase the total project cost by a portion to a meaningful share. For a a seven-figure sum restoration, that represents a a significant investmentto a substantial six-figure sumshortfall if Ordinance or Law coverage is absent or insufficient.

Strategic Navigation of a Claim

When we represent a HNW homeowner or work alongside a premium adjuster, our methodology involves three critical steps:

- Detailed Code Audit: We perform a comprehensive review of the current IRC and local municipal amendments relative to the existing structure. This allows us to identify potential “Coverage C” triggers before the first nail is pulled.

- Structural Valuation: In cases where the Architectural Reconstruction is extensive, we calculate the replacement cost of the undamaged portions of the home to maximize “Coverage A” and “Coverage B” claims.

- Documentary Advocacy: We provide the insurer with the “legal necessity” documentation they require to release funds. This includes citations of specific ordinances and direct correspondence from the building department, leaving no room for the carrier to categorize mandatory upgrades as “discretionary improvements.”

Frequently Asked Questions

Do I have ordinance or law coverage?

You must check your policy declarations page; it is often an elective endorsement rather than a standard inclusion in basic policies. Even if it is included, it is frequently capped at a percentage of the dwelling coverage (e.g., a portion or a meaningful share of Coverage A). For HNW properties, this percentage may need to be significantly higher to cover the true cost of modern compliance.

Is Ordinance or Law coverage the same as “Guaranteed Replacement Cost”?

No. Guaranteed Replacement Cost typically covers the fluctuating costs of labor and materials to rebuild the original structure. Ordinance or Law specifically covers the increased cost of changing the structure to meet new legal standards. You generally need both to be fully protected.

Conclusion: Protecting the Integrity of Your Investment

In the West Metro, luxury homes are more than just residences; they are legacies and significant financial investments. Allowing an insurance company to settle a claim based on outdated building standards is not just a disservice to the property; it is a financial risk that most HNW homeowners cannot afford to take. Ordinance or Law coverage is the mechanism that ensures your home is not just rebuilt, but rebuilt to the standard the law demands.

At Partners Restoration, we combine the precision of a Master Builder with the strategic insight of a Certified Insurance Advocate. We understand the local landscape, we know the “a substantial portion rule” nuances, and we have the expertise to ensure your policy performs exactly as it should during a time of crisis.

Ensure Your Restoration Meets Modern Standards

Don’t leave your rebuild to chance. If you are dealing with a complex claim or want to ensure your current policy provides adequate protection for your West Metro estate, contact us today.

Leave A Comment